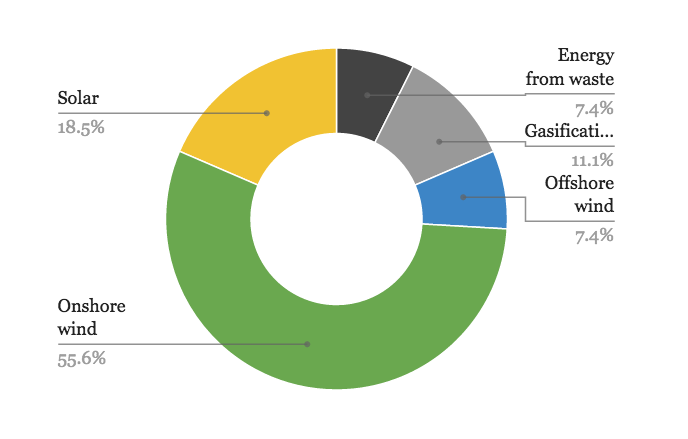

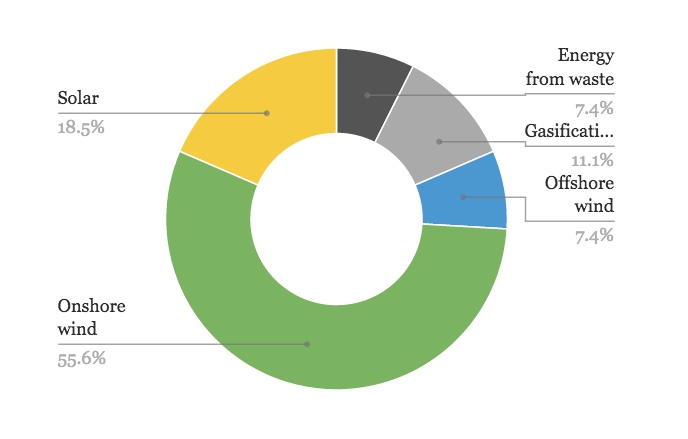

An article in the Telegraph last week highlighted the good news that that economic growth and carbon emissions had “uncoupled”, as the world economy grew 3.3% whilst carbon emissions practically stalled. The UK economy will be further boosted by the growing investment in low-carbon technology, and UK SMEs should aim to grab some of the windfall by implementing alternative sources of power into their businesses where possible. The distribution of UK renewable energy projects is broken down below.

The fast-growing market, which has seen prices drop continually since 2006, has been helped by the improvement in the technology of “green” energy options on offer to customers and businesses in the UK. For instance, even solar energy is proving to be surprisingly successful in the UK, proving to naysayers that had written off the technology as ill-suited to flaky British weather. According to research published in The Guardian, the number of solar installations in the UK almost doubled in 2014.

However, the increase in supply doesn’t always make it cheaper for businesses looking to “go green”. Solar again is the best example: the price of solar photovoltaics (PV) has plunged which has meant the price per watt of electricity is cheaper. However, the government had previously helped install the technology for users of solar powered electricity as well as giving feed-in tariffs, beneficial tax breaks and a handy buy-back of unused power to boot. As these remunerations have been redacted slowly over time, the cost is rising again and SMEs who should be being urged into using green energy are unable to commit financially.

The traditional thinking has been that the affordability of green technology needs to be matched by efficiency that rivals the traditional power sources. However, as efficiency and profitability is enhanced, there is still a need to subsidise the cost and give tax breaks to companies (particularly SMEs) who are using carbon-neutral energy. Avoiding the need to force businesses into over-zealously categorised regulation whilst simultaneously encouraging green energy is something that Amber Rudd and her successors have to prioritise in a bid to ensure that economic growth and carbon emissions stay “uncoupled”. The Telegraph article ends with a stark warning from Bank of England governor Mark Carney that “in the fullness of time, climate change will threaten financial resilience and longer-term prosperity”. The long-term apocalypse that Carney warns us of, namely the inexorable rise of the Earth’s temperatures, can be prevented by near-term solutions that benefit small businesses in the UK.

Last week, the Office for National Statistics (ONS) announced that productivity in the UK grew at the fastest rate in four years, finally exceeding the pre-economic crisis levels of 2007. A rise in productivity is significant because it is seen as a crucial measure of an economy’s strength and future GDP growth, taking in to account living standards, capital and labour resources. For too long the UK has lagged behind the other G7 countries in terms of productivity: this looks set to continue despite the good news, as gains in productivity are offset by persisting low confidence in UK manufacturing. The incoming UK minimum wage hike will also have a marked effect on productivity as labour hours will cost businesses more.

So what is the effect of macroeconomic productivity on small businesses? Productivity is a key measure that the Bank of England uses to determine interest rates, which are currently kept at record lows. There has been a huge amount of speculation as to when the interest rates will be increased and this news should support those who think a rate hike will be sooner rather than later. Small businesses looking to borrow money will be amongst those monitoring the situation, particularly those with loans with a variable rate. However, the Bank of England typically follows the lead of the US Federal Reserve when altering the interest rates, and it is hard to see any great change any time soon. In the current uncertain global financial and geopolitical climate, analysts are not predicting the first rate rise until spring next year. When that does happen, Mark Carney, the Bank of England’s governor, has stated that increases will be “limited and gradual”. Any changes will take time to filter through to the real economy and SMEs in particular.

Increased UK productivity will be good news to the Bank of England

A raise in productivity is undoubtedly a good sign the UK economy is finally dragging itself out of the doldrums, yet we are still 18% worse than we would have been if the pre-crisis productivity rates had been maintained. It is not just a case of everyone working a bit harder; investment in public infrastructure and fiscal policy will be the defining factors that will hopefully see the UK catching up with everybody else. Small businesses can expect to benefit from increased productivity and subsequent better living standards for its workers, but should be carefully monitoring an imminent interest rate hike when budgeting for the next couple of years.

I am aware that there are other cryptocurrencies available on the web, but for the purpose of keeping this article short I have decided to focus on P2P platforms that use Bitcoins. The leading cryptocurrency in terms of worldwide market value, it has been a rocky ride to say the least in its short life to date.

What is Bitcoin? Bitcoin defines itself on its website as “the first decentralized digital currency, directly transferred from person to person without going through a bank.” Advantages include very low processing fees, no frozen bank accounts and worldwide payments. The currency is secured by a group of individuals called miners, who verify transactions in return for newly generated bitcoins. Traditionally, currency valuation is based upon confidence; the assurance that the central bank is good for the money and promises to pay the bearer on demand. The miner system has been exploited in the past; cybercriminals have a very well-established, tested, and long-operating mechanism to perform marginal-cost distributed computing in the form of botnets, which are undermining the currency’s value by enabling them to produce illegal bitcoins.

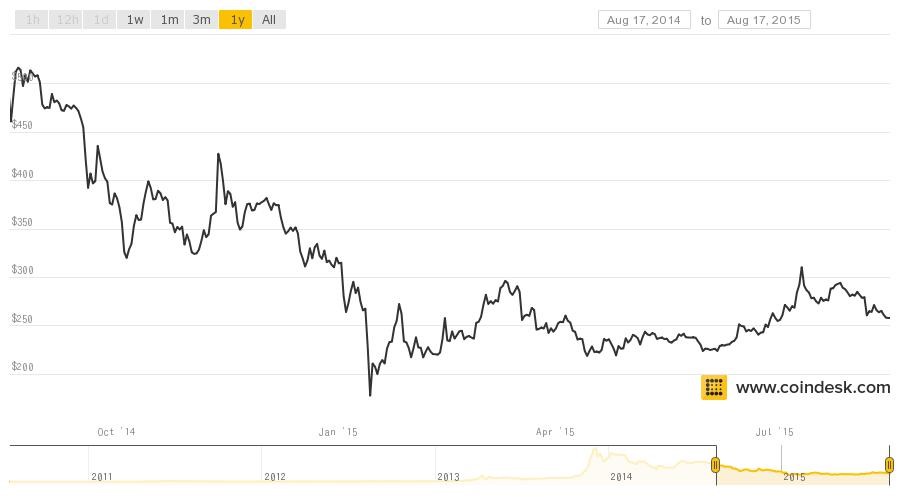

This week, Bitcoin broke through the 215 support level – declining almost 9% in a day.

Another major downside to date has been the currency’s volatility. In its initial stages, bitcoin was still classed as an asset that received bad press due to its link with illegal websites such as The Silk Road. As its reputation and distribution has grown, it has been affected by factors similar to all fiat currencies, as fluctuating perceptions of how to correctly value the currency continue. In the near term, much of the volatility will be driven by investor perception of the ability of gateways to provide a reliable store to secure individual holdings.This week, Bitcoin broke through the 215 support level – declining almost 9% in a day.

Are the risks greater for a potential investor using P2P bitcoin lending platforms?

Bitcoin P2P platforms themselves do not pose more risk than a traditional P2P platform. However, the USP for the P2P lenders to use bitcoin is the ease (both in terms of time and cost) at which money can be transferred overseas. It is here that the risks inevitably begin to stack up. Lending money to borrowers in other countries makes AML and KYC checks nay on impossible. If time is indeed money, then the value saved by cutting out expensive bank fees needs to balance out the time-consuming and ultimately expensive process of vetting potential borrowers. Beware of interest rates that seem too good to be true… they usually are.

A lack of awareness to the risks involved for a potential investor is as dangerous a territory for all unregulated platforms as it is for the investor. P2P lending websites will always be judged by the worst platforms as much as they will the best. The clean, modern P2P cryptocurrency websites do not guarantee clean, modern loans. The regulatory-enforced investment warning signs that adorn the websites of British P2P and B2B lenders are notable in their absence on Bitcoin P2P lending websites. The risks of lending money abroad to markets with conventionally weak currencies should not be understated. If you are borrowing in a highly unstable currency and do not generate revenues in that currency then you create another risk: the exchange rate risk that the cost of the loan, which is unknown to the lender, cannot be met. So what’s the attraction for lenders? Unless they are Bitcoin based, then they are lending to receive an unknown return, which is likely to be less than they expect. To me this is unattractive.

Which platforms should investors be wary of?

Bitbond, based in Germany with offices in the UK and across Europe, specialise in facilitating bitcoin loans to small online business owners to secure funding to increase their inventories and/or revenue. Bitbond launched in July 2013. In its first year of trading it funded more than 180 loans worth over €36,000 ($48,000) to date, and has a user base of approximately 4,100 people from over 100 countries. The website claims that lenders receive an average interest rate of 13%. The loans available on their platform range from a 36 month, bitcoin equivalent to 156 USD loan at 21.3% to a Venezuelan borrower aiming to buy mining equipment, to Bitcoin-equivalent USD10000 loan to a German Borrower purchasing stock for his shop. Bitbond relies on debt collectors and prioritizes the creditworthiness of the applicant and the purpose of the loan, yet there are numerous questionable borrowers that still escape the net and make it to the platform.

BitLendingClub offer a similar service. The majority of their borrowers come from countries with a severely damaged economy, such as Venezuela or Argentina. The service is an alternative source of funding for individuals who don’t have bank accounts but have mobile telephones and are used to making mobile payments. Investors offer competing interests rates from which the borrower can choose to fund the project. A potential lender is left with the complex task of assessing loans where the risks are not homogenised. There doesn’t seem to be any regulation of what is posted on the platform, and the rudimentary risk calculations are very much a guideline rather than a science.

It would take a huge amount of luck to invest frequently and completely avoid a dud borrower. Interestingly, their statistics are given as raw data from which an investor must carry out an independent analysis. In short, these platforms are for experienced, tech-savvy investors, or somebody with few pennies going spare willing to help out an individual in another country, with the hope of seeing some sort of return.

The Bitbond model has been heralded by Cryptocoins News as the most secure way yet of avoiding some of the horror stories that have plagued sights such as BTCjam. The San Francisco-based company specialise in offering personal loans starting from 6.7% percent APR, yet in the same digital “breath” suspiciously offer lenders up to 19.3% APR on their loan. Once again, be wary of offers that seem too good to be true. Their mission statement to “make credit affordable and accessible” is based upon the “accepted wisdom” that interest rates for personal loans in developing countries can exceed 200% per year, choosing Brazil as an example. Brazil, along with India, has certainly been the poster boy for extortionate interest rates in the past, although the issue is certainly being addressed. BankFacil are at the forefront of a new generation of Brazilian financiers that offer secure finance to Brazilians, but still at rates of between 20-30%.

There are horror stories aplenty on internet forums that slate BTCJam: those alone should deter all but the most reckless investor. In an age where borrowing money through unconventional online platforms is more and more common, BTCjam certainly can command even more of a share of the market than they already have. By the end of 2014, BTCjam had facilitated bitcoin loans in excess of $10 million with 100,000 users in over 200 countries… a bold claim considering there are only 196 recognised countries in the world. Such minor discrepancies are important: transparency should be guaranteed, but in the convoluted world of cryptocurrency market places, a fine tooth comb and plenty of due diligence is necessary to enjoy any success as an investor. I for one would avoid them like the plague, impressive as the technology is. One of the good things about loans is that you know what you need to repay. Uncertainty is always unattractive to investors (equity and/or debt). The old maxim that as long as markets are moving somebody is making a profit is true, but only if you can go long and short and do so quickly. A true and perfect market simply doesn’t exist for bitcoin-based crowd loans… so invest at your peril.

The EU is an undemocratic mess that restricts trade and therefore prosperity.

The UK’s trade with the EU is in terminal decline, whereas its trade with the rest of the world is increasing.

The UK should therefore get out before the EU drags it down in to the mire of economic stagnation that currently afflicts the remainder of the member nations.

I agree that the EU is an undemocratic mess that over-regulates and thereby probably restricts trade. The UK joined the then European Economic Community on 1st January 1973. That’s more than 42 (yes, forty two) years ago. The problems occurred on our watch! This was not something that was forced upon the UK last week. This is something that the UK allowed to happen to itself while it was disengaged.

I do not agree, however, that the EU’s economy is in terminal decline… and maybe the stats don’t really say that either. There’s always a risk of fighting the last war when using statistics, which focus retrospectively. While the 2Q15 GDP growth figures for German and France are lacklustre, those for Spain appear to be better. Even as I write now from South-West France I see signs of a recovery, with homeowners beginning to work on their properties once more.

Source: http://bit.ly/1HVvcCD

Our nation’s attitude to the EU has always been to reap the benefits of free trade and avoid the harder stuff, leaving that to the Brussels-based bureaucrats and in the process turning those bureaucrats into bogeyman figures. This is a ridiculous attitude to take. These are our neighbours who have organised a club that we voted in favour of joining. We should have spent the last 42 years helping them, putting our energies into a better EU for all members rather than some form of super membership for the UK. Increased democracy within the EU would strengthen members’ economies by homogenizing trade rules for all.

The notion that the UK can easily replace EU trade partners with members of the Commonwealth is fanciful. That Britain’s international trade has increased in recent years is good news. Britain should therefore, as a member of the EU, push to lower the EU’s trade barriers with the rest of the world. Free trade across the globe is the bedrock of economic prosperity, not free trade for the (British) Commonwealth (Empire). I thought that lesson had been learnt many years ago.

The alternative of negotiating a Swiss type deal with the EU, thereby keeping the vast majority of British EU trade, simply doesn’t ring true with me. I doubt if we take our ball home that former partners would feel goodwill towards us and agree a treaty that is principally for the UK’s benefit. One must also consider that “Brexit” would be a costly, drawn out affair full of legal quagmire and political gridlock. Indeed we can be certain there would be no rush from the EU side, after 42 years of wasting time as a disingenuous member of their club.

The UK is not the only state within the EU that has tried to use the system for its own benefit, to the detriment of others. The two largest economies within the Eurozone are also guilty of this. Germany has imposed on Greece a bailout that is punitive, unworkable and against the diplomatic bonhomie that was intended from its inception, whilst its manufacturers continue to ram under-priced goods down the throats of poorer EU members. France, meanwhile, has always pandered to its farmers and supported the unworkable and unaffordable Common Agricultural Policy.

Yet the opportunity to make the EU more democratic, dramatically lower the hidden trade barriers and form a global hub of economic prosperity still exists. Unfortunately I am not sure that the political will remains. And Britain has wasted its political capital for the last 42 years. However, I would argue that there is still time and that the potential benefits far outweigh the risks.

{kind=link}