[avatar]

This post is made largely in response to an article written by Nicolas Stone for Economics21 and reproduced in CapX, see http://www.capx.co/external/americans-should-urge-brits-to-vote-for-brexit/.

I would summarise the argument put as:

- The EU is an undemocratic mess that restricts trade and therefore prosperity.

- The UK’s trade with the EU is in terminal decline, whereas its trade with the rest of the world is increasing.

- The UK should therefore get out before the EU drags it down in to the mire of economic stagnation that currently afflicts the remainder of the member nations.

I agree that the EU is an undemocratic mess that over-regulates and thereby probably restricts trade. The UK joined the then European Economic Community on 1st January 1973. That’s more than 42 (yes, forty two) years ago. The problems occurred on our watch! This was not something that was forced upon the UK last week. This is something that the UK allowed to happen to itself while it was disengaged.

I do not agree, however, that the EU’s economy is in terminal decline… and maybe the stats don’t really say that either. There’s always a risk of fighting the last war when using statistics, which focus retrospectively. While the 2Q15 GDP growth figures for German and France are lacklustre, those for Spain appear to be better. Even as I write now from South-West France I see signs of a recovery, with homeowners beginning to work on their properties once more.

Our nation’s attitude to the EU has always been to reap the benefits of free trade and avoid the harder stuff, leaving that to the Brussels-based bureaucrats and in the process turning those bureaucrats into bogeyman figures. This is a ridiculous attitude to take. These are our neighbours who have organised a club that we voted in favour of joining. We should have spent the last 42 years helping them, putting our energies into a better EU for all members rather than some form of super membership for the UK. Increased democracy within the EU would strengthen members’ economies by homogenizing trade rules for all.

The notion that the UK can easily replace EU trade partners with members of the Commonwealth is fanciful. That Britain’s international trade has increased in recent years is good news. Britain should therefore, as a member of the EU, push to lower the EU’s trade barriers with the rest of the world. Free trade across the globe is the bedrock of economic prosperity, not free trade for the (British) Commonwealth (Empire). I thought that lesson had been learnt many years ago.

The alternative of negotiating a Swiss type deal with the EU, thereby keeping the vast majority of British EU trade, simply doesn’t ring true with me. I doubt if we take our ball home that former partners would feel goodwill towards us and agree a treaty that is principally for the UK’s benefit. One must also consider that “Brexit” would be a costly, drawn out affair full of legal quagmire and political gridlock. Indeed we can be certain there would be no rush from the EU side, after 42 years of wasting time as a disingenuous member of their club.

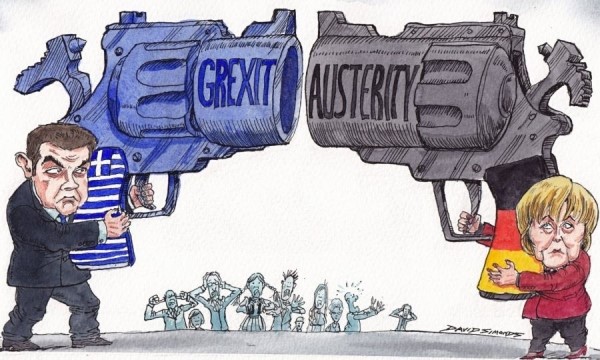

The UK is not the only state within the EU that has tried to use the system for its own benefit, to the detriment of others. The two largest economies within the Eurozone are also guilty of this. Germany has imposed on Greece a bailout that is punitive, unworkable and against the diplomatic bonhomie that was intended from its inception, whilst its manufacturers continue to ram under-priced goods down the throats of poorer EU members. France, meanwhile, has always pandered to its farmers and supported the unworkable and unaffordable Common Agricultural Policy.

Yet the opportunity to make the EU more democratic, dramatically lower the hidden trade barriers and form a global hub of economic prosperity still exists. Unfortunately I am not sure that the political will remains. And Britain has wasted its political capital for the last 42 years. However, I would argue that there is still time and that the potential benefits far outweigh the risks.