Following on from the two posts that explain equity and reward based crowdfunding, we move on to debt-based crowdlending, also known as Peer to Peer (P2P) lending, sometimes Market Place lending and in FCA speak as debt based investing. For brevity I’ll use P2P, although this is somewhat confusing as some of the borrowers are businesses, or P2B. A newcomer to alternative finance, whether it be through conversation or news, is more likely to have heard of crowdfunding, largely due to press interest in that specific area of FinTech and in particular the innovative crowd raises that businesses and individuals have employed. Yet in the UK, the P2P lending industry is worth just under £4.5 billion, compared to £132.5 million cumulative total raised through crowdfunding. Borrowers are attracted by a less clunky process that is competitively priced and easy to use. The vast range of alternative finance solutions available means that both businesses and consumers can find a loan tailored to their needs. Lenders, meanwhile, are drawn to the sweet spot of statistically lower risk investment at interest rates that go beyond the bounds of anything offered by a bank.

The P2P lending sphere can be broadly broken down into three categories: P2P consumer loans, P2P business loans and invoice financing. The biggest player in the consumer loans market is Zopa, who are the oldest and arguably the biggest alternative finance company in the world. They have lent over £1 billion to consumers at an average loan size of £7,500, offering investors a return of 5%. Every consumer loans company is only as good as their borrowers; Zopa have reported 0.04% actual defaults so far this year, a figure which is made even lower by the Zopa Safeguard Trust which helps pay-out in case of bad debts. The fund is taken from the fee that each borrower pays when their loan is approved. Another of the major P2P consumer lenders, RateSetter, have their own provision fund to help bail out lenders to borrowers who have defaulted. RateSetter operate a platform that allows lenders and borrowers to pair up through a process of bidding, over four set term lengths. The model has proved very popular with both individuals who appreciate the transparency of the loan structure and lenders enjoy decent interest rates. RateSetter also offer business loans in the region of £25k to £1 million.

The business lending market is diverse for both investors and borrowers; loan size, terms, length, funding and structure vary from platform to platform. Just dipping a toe into the water in terms of range and variety, you can facilitate finance for property loans through Assetz Capital, Wellesley have their own listed bond that offer lenders 4.75% per annum over three years or 5.5% per annum over five, Folk to Folk specialise in regional lending in the South-West, Landbay secure lenders’ money against residential mortgages, MarketInvoice and Platform Black allow investors to access funds in outstanding invoices and factoring. The list goes one: the Best place to explore the full array of P2P operators and the services they provide is on the AltFi news website. The banks do not appear to have the will or resources to compete, despite their own admission that most of the platforms are supplying an updated version of services that they have provided for years.

Mitigate the risks and P2P Lending is a fantastic way to save wisely whilst helping SMEs and consumers drive UK economic growth. The incoming Alternative Finance ISA will bring in a whole host of new lenders; it is crucial that the industry is properly regulated and that platforms adapt sufficiently to ensure that the optimism continues.

I am aware that there are other cryptocurrencies available on the web, but for the purpose of keeping this article short I have decided to focus on P2P platforms that use Bitcoins. The leading cryptocurrency in terms of worldwide market value, it has been a rocky ride to say the least in its short life to date.

What is Bitcoin? Bitcoin defines itself on its website as “the first decentralized digital currency, directly transferred from person to person without going through a bank.” Advantages include very low processing fees, no frozen bank accounts and worldwide payments. The currency is secured by a group of individuals called miners, who verify transactions in return for newly generated bitcoins. Traditionally, currency valuation is based upon confidence; the assurance that the central bank is good for the money and promises to pay the bearer on demand. The miner system has been exploited in the past; cybercriminals have a very well-established, tested, and long-operating mechanism to perform marginal-cost distributed computing in the form of botnets, which are undermining the currency’s value by enabling them to produce illegal bitcoins.

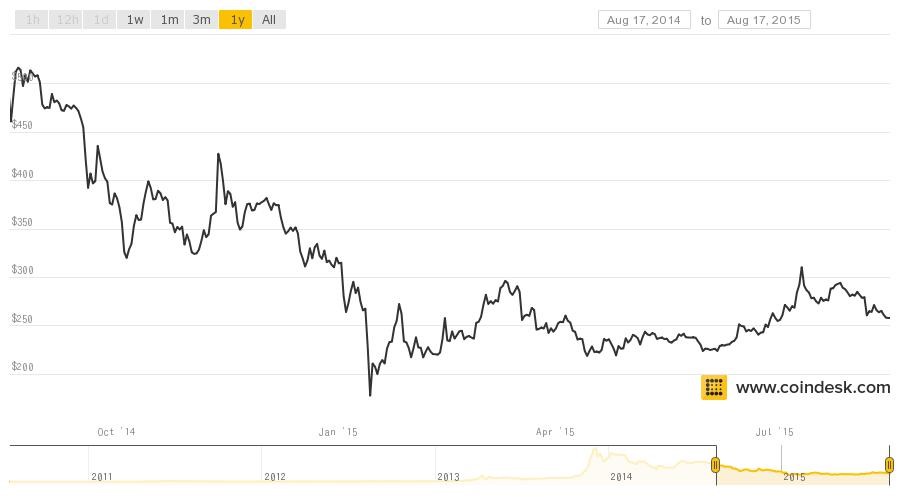

This week, Bitcoin broke through the 215 support level – declining almost 9% in a day.

Another major downside to date has been the currency’s volatility. In its initial stages, bitcoin was still classed as an asset that received bad press due to its link with illegal websites such as The Silk Road. As its reputation and distribution has grown, it has been affected by factors similar to all fiat currencies, as fluctuating perceptions of how to correctly value the currency continue. In the near term, much of the volatility will be driven by investor perception of the ability of gateways to provide a reliable store to secure individual holdings.This week, Bitcoin broke through the 215 support level – declining almost 9% in a day.

Are the risks greater for a potential investor using P2P bitcoin lending platforms?

Bitcoin P2P platforms themselves do not pose more risk than a traditional P2P platform. However, the USP for the P2P lenders to use bitcoin is the ease (both in terms of time and cost) at which money can be transferred overseas. It is here that the risks inevitably begin to stack up. Lending money to borrowers in other countries makes AML and KYC checks nay on impossible. If time is indeed money, then the value saved by cutting out expensive bank fees needs to balance out the time-consuming and ultimately expensive process of vetting potential borrowers. Beware of interest rates that seem too good to be true… they usually are.

A lack of awareness to the risks involved for a potential investor is as dangerous a territory for all unregulated platforms as it is for the investor. P2P lending websites will always be judged by the worst platforms as much as they will the best. The clean, modern P2P cryptocurrency websites do not guarantee clean, modern loans. The regulatory-enforced investment warning signs that adorn the websites of British P2P and B2B lenders are notable in their absence on Bitcoin P2P lending websites. The risks of lending money abroad to markets with conventionally weak currencies should not be understated. If you are borrowing in a highly unstable currency and do not generate revenues in that currency then you create another risk: the exchange rate risk that the cost of the loan, which is unknown to the lender, cannot be met. So what’s the attraction for lenders? Unless they are Bitcoin based, then they are lending to receive an unknown return, which is likely to be less than they expect. To me this is unattractive.

Which platforms should investors be wary of?

Bitbond, based in Germany with offices in the UK and across Europe, specialise in facilitating bitcoin loans to small online business owners to secure funding to increase their inventories and/or revenue. Bitbond launched in July 2013. In its first year of trading it funded more than 180 loans worth over €36,000 ($48,000) to date, and has a user base of approximately 4,100 people from over 100 countries. The website claims that lenders receive an average interest rate of 13%. The loans available on their platform range from a 36 month, bitcoin equivalent to 156 USD loan at 21.3% to a Venezuelan borrower aiming to buy mining equipment, to Bitcoin-equivalent USD10000 loan to a German Borrower purchasing stock for his shop. Bitbond relies on debt collectors and prioritizes the creditworthiness of the applicant and the purpose of the loan, yet there are numerous questionable borrowers that still escape the net and make it to the platform.

BitLendingClub offer a similar service. The majority of their borrowers come from countries with a severely damaged economy, such as Venezuela or Argentina. The service is an alternative source of funding for individuals who don’t have bank accounts but have mobile telephones and are used to making mobile payments. Investors offer competing interests rates from which the borrower can choose to fund the project. A potential lender is left with the complex task of assessing loans where the risks are not homogenised. There doesn’t seem to be any regulation of what is posted on the platform, and the rudimentary risk calculations are very much a guideline rather than a science.

It would take a huge amount of luck to invest frequently and completely avoid a dud borrower. Interestingly, their statistics are given as raw data from which an investor must carry out an independent analysis. In short, these platforms are for experienced, tech-savvy investors, or somebody with few pennies going spare willing to help out an individual in another country, with the hope of seeing some sort of return.

The Bitbond model has been heralded by Cryptocoins News as the most secure way yet of avoiding some of the horror stories that have plagued sights such as BTCjam. The San Francisco-based company specialise in offering personal loans starting from 6.7% percent APR, yet in the same digital “breath” suspiciously offer lenders up to 19.3% APR on their loan. Once again, be wary of offers that seem too good to be true. Their mission statement to “make credit affordable and accessible” is based upon the “accepted wisdom” that interest rates for personal loans in developing countries can exceed 200% per year, choosing Brazil as an example. Brazil, along with India, has certainly been the poster boy for extortionate interest rates in the past, although the issue is certainly being addressed. BankFacil are at the forefront of a new generation of Brazilian financiers that offer secure finance to Brazilians, but still at rates of between 20-30%.

There are horror stories aplenty on internet forums that slate BTCJam: those alone should deter all but the most reckless investor. In an age where borrowing money through unconventional online platforms is more and more common, BTCjam certainly can command even more of a share of the market than they already have. By the end of 2014, BTCjam had facilitated bitcoin loans in excess of $10 million with 100,000 users in over 200 countries… a bold claim considering there are only 196 recognised countries in the world. Such minor discrepancies are important: transparency should be guaranteed, but in the convoluted world of cryptocurrency market places, a fine tooth comb and plenty of due diligence is necessary to enjoy any success as an investor. I for one would avoid them like the plague, impressive as the technology is. One of the good things about loans is that you know what you need to repay. Uncertainty is always unattractive to investors (equity and/or debt). The old maxim that as long as markets are moving somebody is making a profit is true, but only if you can go long and short and do so quickly. A true and perfect market simply doesn’t exist for bitcoin-based crowd loans… so invest at your peril.

In the UK there has been a notable shift in the P2P Lending model over the last year towards increased involvement from institutional investors. The UK market is sometimes said to be two years behind the US P2P market, and this statement certainly holds true when it comes to attracting funds from this class of investor. Indeed, in the US it is estimated that around 80% of loans made through the two largest platforms, Lending Club and Prosper, are currently taken by institutional investors replacing the retail lenders that previously dominated the space.

There are two principal explanations for this shift beginning to occur in the UK: firstly, institutions are seeking access to new asset classes, and secondly, institutions see in P2P a scalable opportunity. Return is also key. With record low interest rates, volatile stock markets, and low bond yields, the P2P lending space offers investors the chance to earn considerably better returns without a proportionate increase in risk – an undeniable positive.

Thus far there have already been some high profile institutional involvements. In October, Eaglewood Capital finalized a $75 million securitization of P2P loans that were originated by Lending Club. In addition to this, Funding Circle has done a deal with KLS Diversified Asset Management, a US fixed income fund, to lend £132 million to UK businesses. This is the first time a US investment firm has lent money to British business on a P2P platform, further proof that the UK lending model is following the trends in the US but also that institutional money in the UK is not solely limited to UK institutions.

There is an obvious argument that institutional involvement could signify the end of ‘P2P’ and the ‘democratisation of finance,’ but in the author’s opinion this is simply not the case. Firstly, institutional involvement signifies an extra layer of due diligence, a form of due diligence that individuals are realistically unlikely to have available. This allows individuals to follow the smart money. Furthermore, the weight of additional institutional capital allows for larger loans to be funded over platforms, allowing more businesses to gain access to the financing they are sorely lacking. Lastly, it allows platforms to scale and reach targets at a far superior rate to relying on retail investment alone. In short, everyone’s a winner.

So whilst institutional money may currently represent only 30% of P2P funds in the UK, I expect that figure to be much, much higher in 2015.

The advent of the peer-to-peer model has brought fundamental change to the lending industry; change which has seen platforms such as ArchOver move with the zeitgeist and embrace the internet as a medium through which to fund loans to businesses and individuals. But as the peer-to-peer space has begun to mature and take root, much change has begun to occur within the sector itself, with many platforms emerging with their own specific applications for the peer-to-peer model.

One interesting entrant which certainly captures the ‘forward-looking’ character of the sector is Abundance Generation, a platform which provides funding to eco-friendly projects throughout the UK. Investors buy debentures in the projects listed on the platform, which have included wind farms and solar energy initiatives, with different projects carrying different rates of return. The platform seems to have successfully tapped into modern sensitivities surrounding global warming and the viability of fossil-fuel use in the longer term, with investors having pledged just over £8m on the platform at the time of writing.

Another entrant whose focus is equally timely is Bitbond. This German platform, mentioned by James in his recent blog, is a peer-to-peer business lender that solely uses the digital currency Bitcoin. The platform takes the concept of ‘disintermediation’ and the diminishing role of the banks in finance a stage further than most, for even a bank account is not required to lend and borrow on the platform. Indeed, Bitbond’s website carries the tagline “banking is necessary, banks are not,” which neatly illustrates the ethos driving their unusual platform and its use of a digital cryptocurrency.

Bitbond’s belief in the potential of digital technology is mirrored in the offering of Pollen vc, a platform with offices in both the UK and US. Pollen seeks to address the financing problems faced by developers creating apps for Google Play and Apple’s App Store. These developers not only face fierce competition for the attention of consumers, but also a long delay between making sales in the marketplaces and receiving payment. Pollen aims to alleviate the cash flow problems that this can cause by monitoring sales data and advancing a percentage of their clients’ earned revenue to allow them to continue developing their apps. To complement this service, Pollen’s management also aim to consult with them to offer advice on exactly how they should move forward with their products.

Taken together, these three platforms serve as an excellent illustration of the growing diversity found within the peer-to-peer space. And in the author’s opinion, this can only bode well for the sector at large.